Introduction

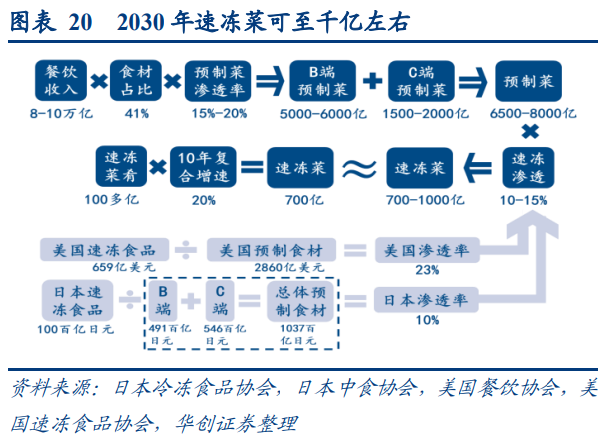

It is estimated that the scale of Chinese catering industry will exceed 10 trillion yuan in 2030. Assuming that the conservatively calculated penetration rate of prefabricated vegetables is raised to 15-20% (currently 10-15%) based on 8 trillion yuan, the scale of the B end is 500 billion yuan, and the C end is estimated to be 700 billion yuan, with a compound growth rate of 13%.

In the future, with the entry of leading enterprises, the pattern of concentration will gradually become the main line, and strong competitive enterprises will have more advantages.

01

Business essence: improving efficiency

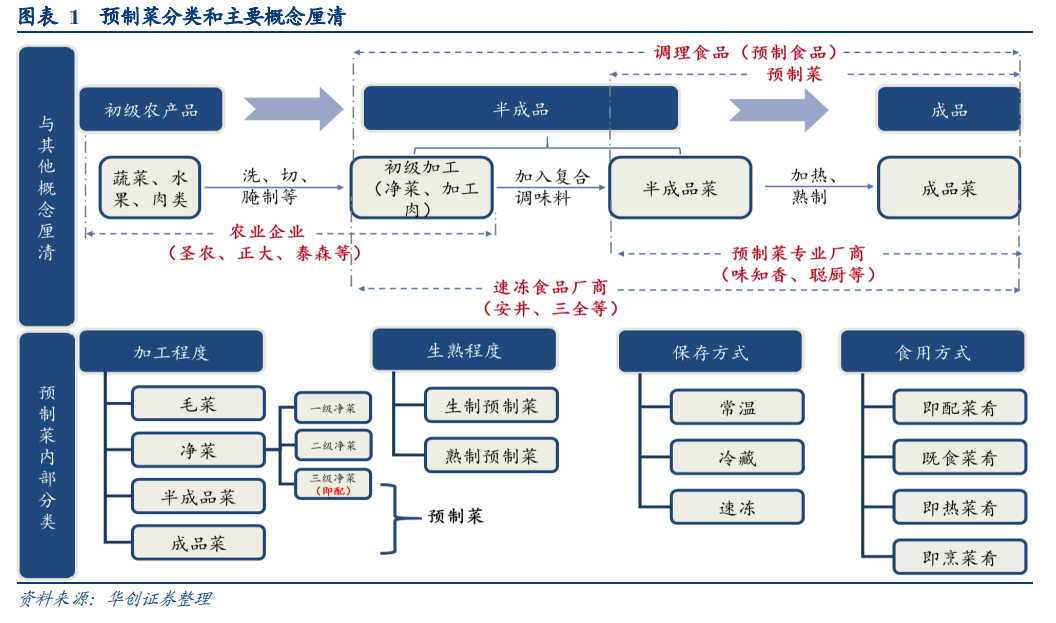

Conceptually, prefabricated dishes belong to the category of prepared foods, with the core being dishes.

Prefabricated dishes refer to finished or semi-finished products made from agricultural, livestock, poultry, and aquatic products as raw materials, supplemented by various auxiliary materials, and processed in advance. Compared to current cooking, prefabricated dishes need to be processed in advance, but they are still "dishes" in nature. They are different from ordinary processed foods, with a shorter shelf life and fresh ingredients.

From the perspective of commercial attributes, prefabricated dishes belong to the category of catering industry, and scale is the key.

First, it is necessary to distinguish the business attributes of food and catering. The essence of the food business is to sell products, while catering is more about selling services. The distance from consumers is different, and the degree of influence of human factors is different. Usually, human factors can amplify the instability of business systems.

In traditional Chinese restaurants, the change of chefs may determine the amount of customer flow. Because catering can meet people's higher level needs.

However, in standardized food production, the human factor is eliminated as much as possible, resulting in higher business scalability, concentration, and demand stability.

With the upgrading of technology and demand, catering and food go hand in hand, and prefabricated dishes emerge as the times require.

As a product of the integrated development of catering and food, prefabricated dishes maximize industrialization and expansion under guaranteed taste conditions, achieving optimal efficiency to some extent.

02

Market size: 700 billion yuan in the next decade

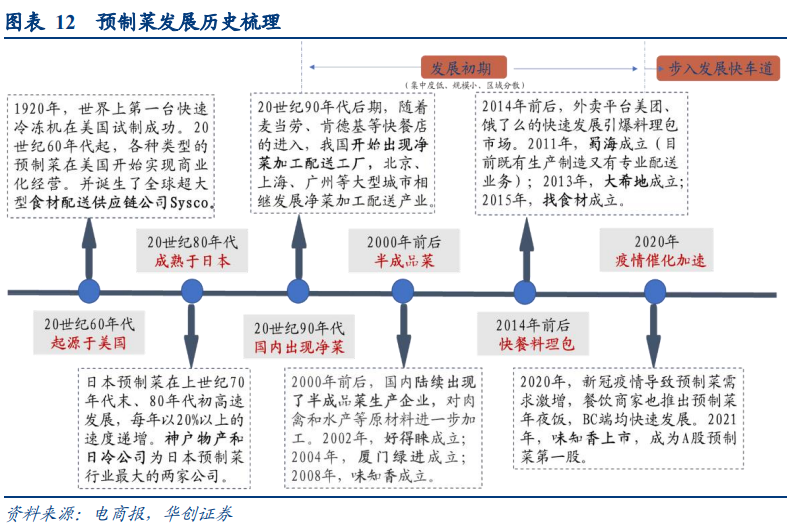

Prefabricated dishes originated in the United States and began to be commercialized in the 1960s.

In the late 1970s, with the rapid development of the Japanese economy, prefabricated dishes experienced a rapid growth of over 20% in Japan.

After the 1990s, with the entry of fast food restaurants such as McDonald's and KFC, clean vegetable distribution and processing plants began to appear in China. After 2000, enterprises engaged in deep processing of semi-finished vegetables began to emerge, but due to immature conditions, the overall development of the industry is still relatively slow.

After 2014, with the economic development and explosive growth of takeout, B-end consumption entered a period of expansion. By 2020, Y-end consumption was blocked due to Y-situation, and restaurants actively sold their dishes in the form of semi-finished products. In addition, the outbreak of residential consumption directly catalyzed the acceleration of C-end consumption.

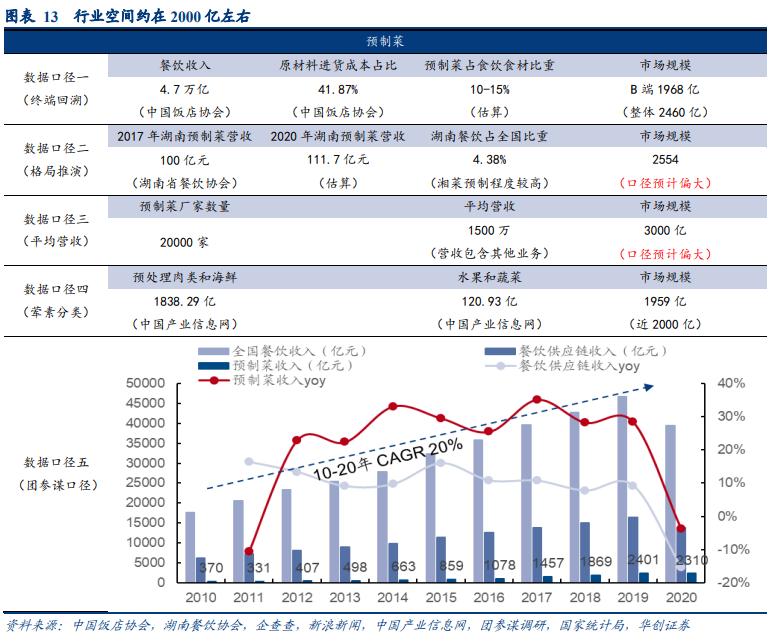

Huachuang Securities estimates that, on the whole, the current scale of China's prefabricated vegetable market is about 200 billion, including 180 billion for the B end and 40 billion for the C end. The compound growth rate has remained around 20% in the past decade, with a compound growth rate of around 30% from 2014 to 2019.

Currently, China's annual per capita food and beverage consumption is 3500 yuan, and the food and beverage externalization rate is 35%, while the United States and Japan are both around 45%. Driven by the accelerated pace of life and economic development, China's food and beverage development has full potential.

According to the "Five Year (2021-2025) Work Plan of the China Cuisine Association", it is estimated that the scale of Chinese catering industry will exceed 10 trillion yuan in 2030. Assuming that the conservatively calculated penetration rate of prefabricated dishes is raised to 15-20% (currently 10-15%) based on 8 trillion yuan, the scale of the B-end is 500 billion yuan, and the C-end is expected to be 700 billion yuan, with a compound growth rate of 13%. Referring to the penetration rate of quick-frozen vegetables in the United States and Japan, assuming that it is 10-15% in China, the scale of quick-frozen prefabricated vegetables is expected to be around 100 billion yuan.

03

Reorganization of overseas pattern

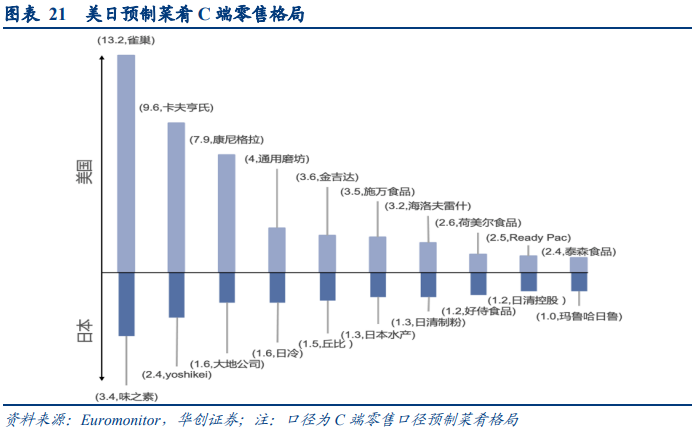

Currently, the overseas market pattern of prefabricated vegetables is becoming fragmented.

Due to the higher complexity of prefabricated dishes compared to frozen foods, it is difficult for companies to dominate even in the United States and Japan, which is more reflected in the differentiated competition of segmented tracks.

In the United States, Nestle, Kraft Heinz, and ConAgra are mainly staple foods, while Tyson and Dutch styles are mainly meat based. In Japan, in addition to traditional quick-frozen leading enterprises, there are also box lunch leading enterprises such as Fulinas. In addition, quick-frozen food producers, retail enterprises, and agricultural companies also widely participate.

Moreover, in contrast, the concentration of American leading enterprises is higher, presumably due to factors such as their ability to acquire and eat simply.

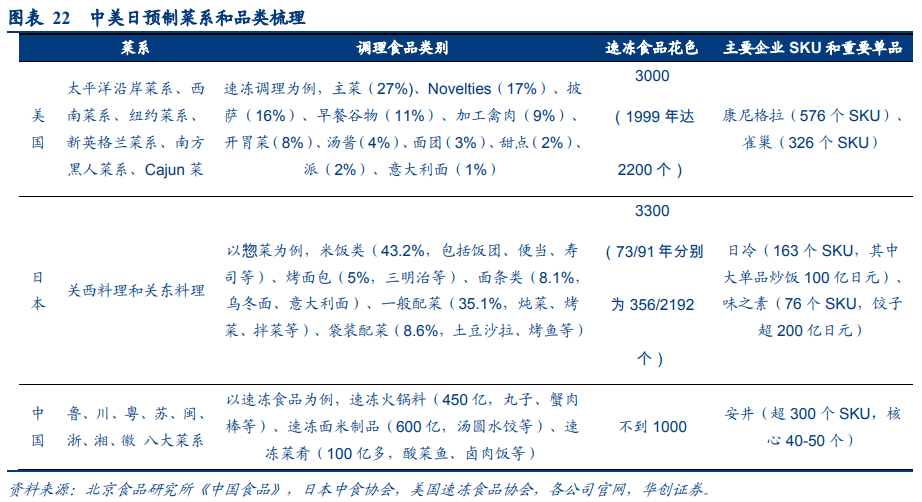

Due to racial diversity, the corresponding cuisines in the United States are also relatively rich, and currently the mainstream cuisines are classified according to geographical location. Due to the small territory of Japan, the cuisine is divided into Kansai and Kandong cuisine.

On the whole, the categories in the United States and Japan are relatively complex, with more dishes in China compared to the main categories in the United States and Japan. Considering that China has a larger market scale, there is more room for exploration in the future.

Sorting out the leading enterprises of overseas prefabricated dishes, the core players are mainly frozen food merchants and store retailers.

For frozen products manufacturers, quick freezing technology has better solved the problems of short shelf life and low standard product rate of prefabricated vegetables, improving the possibility of large-scale operation of channels. Due to the limited transportation distance and short shelf life of refrigerated and room temperature prefabricated vegetables, they will be more borne by the store type in the future (they can be directly matched to meet the shelf life requirements). However, due to the relatively scattered downstream channels in China, it is difficult for retail brands to break away from the channel boundary, presenting a more regional competitive state.

Currently, China's prefabricated dishes are experiencing a rapid increase in penetration, with dividends and mutual prosperity. In the future, as the number of participants increases and the industry penetration gradually slows, they will enter the shuffle stage after a certain point in time.

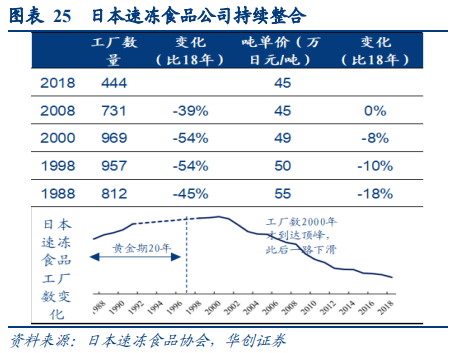

After the end of the golden period in the 1990s, the number of frozen food factories in Japan peaked in 2000, and then entered a brutal reshuffle stage. In 2018, the number of frozen food factories fell to half of the peak. Leading enterprises relied on efficient operation to resist the pressure of price war, and ultimately the winner took all, while the remaining one was king. By 2018, the industry's CR3 was about 60%.

In terms of corporate decision-making, the United States and Japan also have many differences. The United States is good at horizontal mergers and acquisitions, relying on multi brand operations, and taking profit orientation as the criterion. Japan is accustomed to vertical extension, with products and upstream and downstream supporting facilities to the extreme.

04

Early stage of development: scale is king

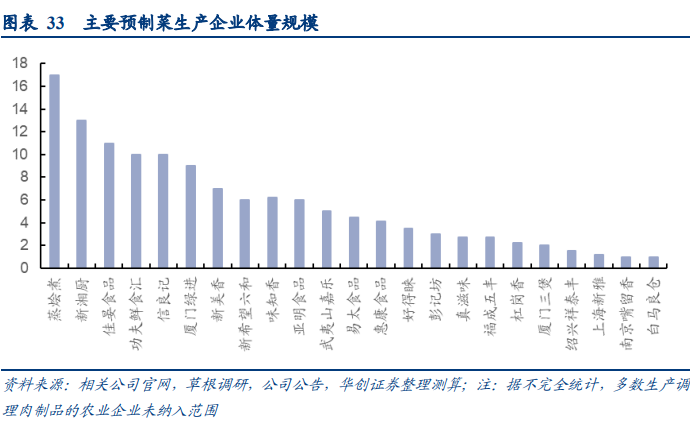

At present, the main leaders of China's prefabricated food industry have basically reached a scale of 1 billion, including steamed stew, Cong Chef (Xinxiang Chef), Jiayan Food, Xiamen Lvjin, and Xin Liangji. However, compared to the market space of 200 billion yuan, the market pattern is extremely fragmented. In addition, there are many enterprises at the level of 100 million yuan, with an average enterprise size of about 15 million in the industry, and they mostly undertake the task of acting as factories.

Enterprises in the industrial chain can be divided into four major genres based on the underlying genes: professional prefabricated vegetable manufacturers (including frozen food manufacturers), catering enterprises, upstream agricultural enterprises, and retail enterprises.

1) Professional manufacturers: They have a product oriented mindset, are good at creating popular products, channel construction, and have advantages in terms of scale. However, there are also differences between 2B and 2C enterprises. 2C enterprises are good at maintaining brands, but not good at point-to-point service development, while 2B enterprises are just the opposite;

2) Catering enterprises: They naturally have a service-oriented mindset and have advantages in dish research and development, brand premium, and store membership groups. However, packaged food operations require pre investment in the early stages, testing the enterprise's channel construction and service capabilities. The difficulty lies in the transformation of thinking and team building in the middle;

3) Retail enterprises: They have a high product richness, are primarily asset oriented, are good at consumer insight and use data driven, and have retail thinking behind them. However, their disadvantages are that quality is difficult to control and products are difficult to exit their own platforms;

4) Upstream agricultural enterprises: Agricultural enterprises have natural advantages in the development of prefabricated vegetables due to their mastery of the upstream and their rich channels of relying on the accumulation of agricultural and livestock products. However, the problem remains how to balance the relationship between 2B and 2C, as well as between new and old products.

In terms of downstream channels, enterprises can choose either B or C channels based on their developability and demand stability, with B-end traffic and C-end brand establishment. Channels with low development difficulty, relatively fixed demand, and high viscosity are more likely to be shipped.

1) Township chefs: Floating chefs who are engaged in weddings and funerals in villages and towns, with a fixed category and a large share. The host of the banquet orders dishes. There are usually township chefs associations (key figures) in the local area, which are prone to generate public praise within the group and require dealers to sink.

2) Hotel: The banquet is ordered by the host, and the product threshold is high. There is a need to provide a wide range of options from 20 to 30, and there is a demand for customization. The service requirements are high, with a certain seasonality. It is difficult to develop but low maintenance costs, and has a first-mover advantage.

3) Group meal: The products are relatively fixed and the procurement planning is strong. Group meal enterprises decide the menu, pay special attention to food safety, and use more third-party products. Development has a first mover advantage.

4) Chain fast food: It is difficult to develop. Most brand chain stores have their own central kitchens, and only advantageous single items have the opportunity to enter. The overall development should be based on the thinking of key customers, and the expanded categories are easily replaced by their own central kitchens. More than 74% of domestic chain catering enterprises have built their own central kitchens, and more than half of them are developing standardized finished products and prefabricated dishes.

5) Small and medium-sized catering: The market space is vast, and the proportion of finished products is high, but the relative demand is relatively scattered. The core idea should give priority to cost, and the channel stickiness is extremely low.

6) Agricultural market: The demand is stable, and the purchasing group is mainly middle-aged and elderly. However, in terms of products, it is necessary to avoid price comparison effects. The back-end tests the supply chain distribution strength and consumer brand recognition.

7) KA and BC supermarkets: The proportion of finished products is high, and the development and operation threshold is also high, which tests professional channel management and brand building. Unlike ordering production based on demand at the B-end, there is a high risk of mismatching production and sales through supermarket channels.

8) Online: The overall volume is still small, supply chain issues are difficult to solve, and development needs to be driven by explosive thinking

05

Segmented circuit

In the prefabricated dishes competition track, Huachuang Securities has refined four categories of tracks: cooking bags, hotel dishes, conditioned meat products, and C-end tracks.

1. Cuisine package: small B starts with market-oriented competition

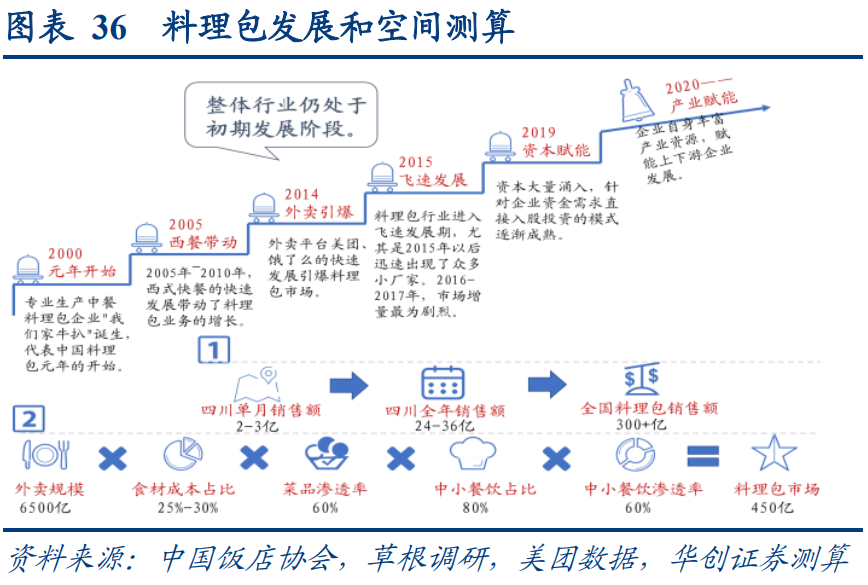

The development of the food and beverage industry is deeply influenced by the general trend of catering. In 2005-2010, the development of Western style fast food led to the growth of food and beverage, and then went deep into Chinese style fast food. From 13-15 years, with the rapid development of online takeout, the food and beverage industry also entered a golden period of development, with the most dramatic market growth in 16-17 years.

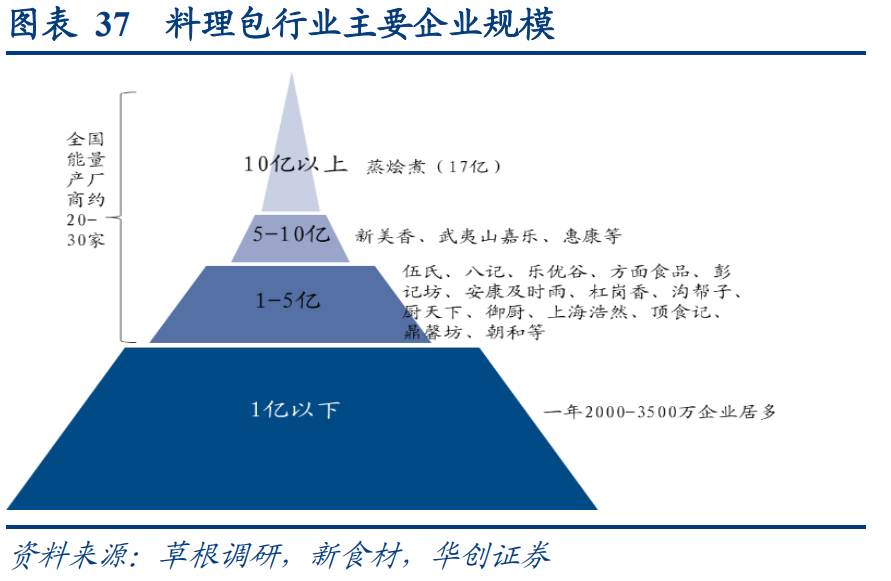

At present, the market is mainly dominated by professional cooking bag manufacturers, such as steamed stew, Xinmeixiang, Huikang, etc. In addition, some agricultural enterprises have entered this circuit, such as Shengnong, which has established a dedicated factory for Chinese cuisine, with a design capacity of 30000 tons, and its main products are 24 types of Chinese cuisine bags.

The downstream of the catering package is mainly connected to small restaurants, and there are no factors such as large-scale catering development relying on customer relationships, self built central kitchen reverse substitution, etc. The overall competition is relatively market-oriented, and regional leaders can form a strong advantage relying on local channel networks. According to different caliber, Huachuang Securities estimates that the national scale is around 50 billion.

Compared to other prefabricated dishes, the profit margin level of the catering factory is only slightly higher than that of the general OEM factory, with a gross profit margin of 20-25% and a net profit margin of around 5%.

The core concern of downstream customers lies in cost, and product prices are relatively transparent, which can rely on scale advantages to achieve share crowding. Moreover, it is easier for a single customer to centrally purchase from the same manufacturer, and customer relationships are easy to establish, but not strong in stickiness, which can easily lead to price wars. The difficulty in research and development is not high, but in the future, the industry needs to strengthen standardization and quality control.

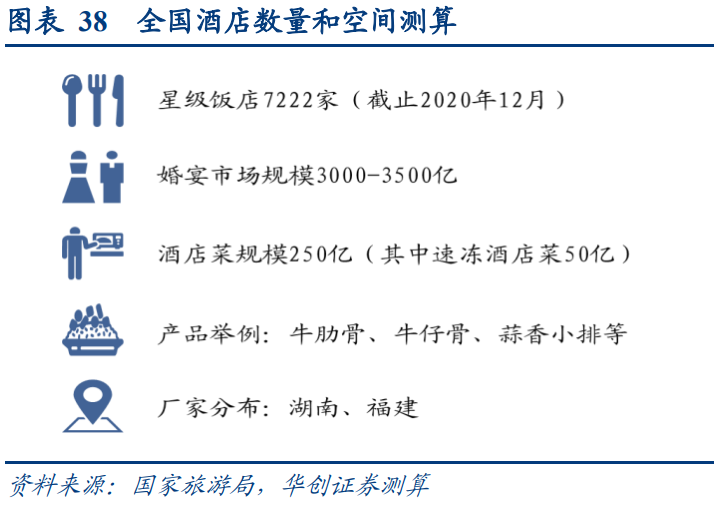

Hotel cuisine: high barrier, high profit track

Hotel dishes are mainly semi-finished dishes, and hotel chefs reprocess them on this basis. They have high requirements for product appearance and taste, relatively high profitability, and high overall barriers to entry. The competitive pressure is weaker than that of cooking and packaging tracks.

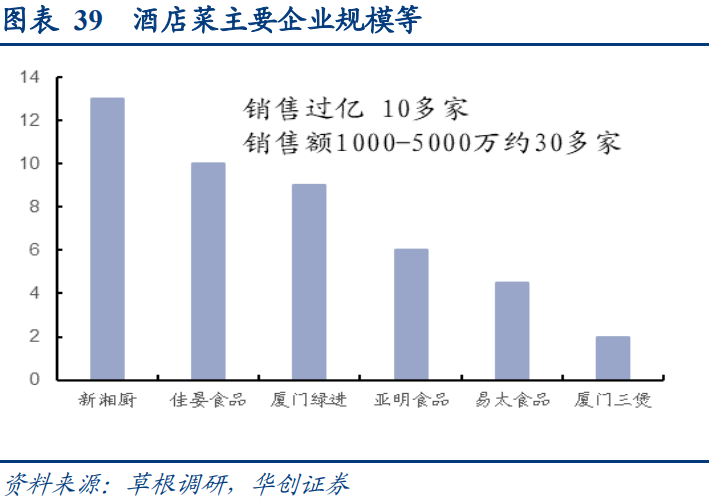

Currently, the main players include quick-frozen hotel dishes enterprises, such as Lujin and Yaming in Fujian, as well as room temperature/refrigerated hotel dishes, such as Xinxiang Kitchen and Jiayan Food in Hunan. In addition, large catering enterprises have also entered relying on their research and development advantages. Hotel dishes are mostly used in banquet markets, etc. Assuming a penetration rate of around 15-20% (slightly higher than the industry), it is estimated that the scale of hotel dishes will be around 25 billion, of which the scale of frozen hotel dishes will be over 5 billion.

The competitive factors include research and development strength, channel services, and obvious first-mover advantages in development. Later development requires enhancing category expansion capabilities. The development of hotel dishes is a big B-end development logic that requires point-to-point service expansion, increased terminal services and guidance, and high requirements for product appearance and quality. Enterprise entry requires certain research and development capabilities. Early development is difficult, but later maintenance costs are low, and advanced entrants have a certain first-mover advantage. However, considering that the categories required for hotel procurement are often difficult to meet in one company, subsequent companies need to enhance their ability to penetrate and expand categories in a single hotel.

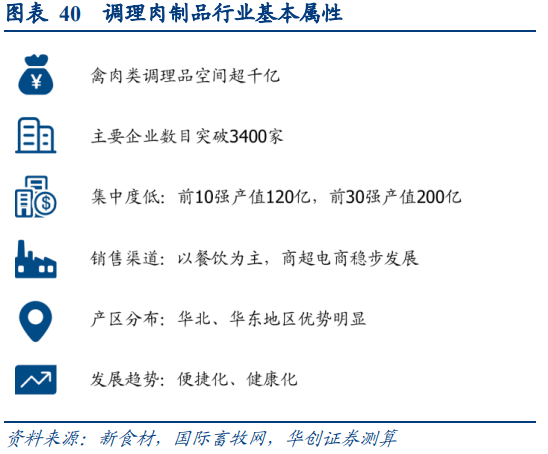

3. Conditioning meat products: Large space, easy to operate, and agricultural enterprises have advantages

The space for meat products in China is about 2 trillion yuan, including 100 billion yuan for conditioning meat products.

Meat products have a wide space and many categories. Conditioning meat products refer to non ready to eat meat products formed by rolling, mixing, seasoning and pre heating. Common products include meat and bone, chicken fillet, Orleans chicken wings, oil consuming beef fillet, crystal shrimp, etc. According to a special survey conducted by Shandong Lvwo, a new food ingredient company in the past 19 years, there are about 3400 poultry and meat conditioning companies nationwide, with an output value exceeding 100 billion, among which the top 50 companies are above 23 billion.

Conditioned meat products are mainly semi-finished products, and terminal operations are relatively easy. Agricultural enterprises are deploying in succession. Upstream raw materials are the key to competition. Compared to other types of prefabricated dishes, the degree of processing of processed meat products is reduced, and the composition of ingredients is less. Therefore, it is simpler in terminal operation and more popular in application.

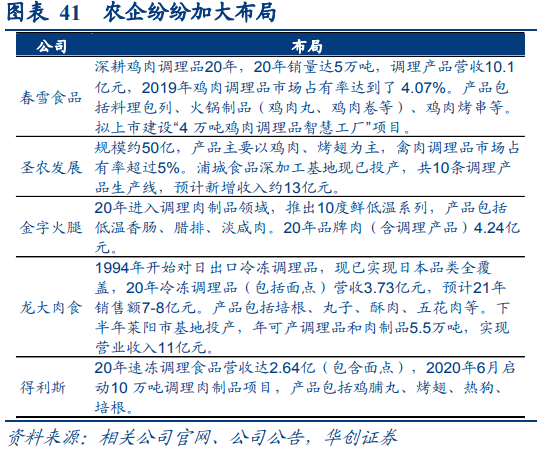

Currently, the main players are meat products or agricultural enterprises, such as Shengnong, Zhengda, Longda Meat, Fengxiang, Delis, Huaying, etc. In addition to cost advantages and channel efficiency, upstream raw materials are also the core competitive points in terms of competitive factors. Therefore, agricultural enterprises have natural advantages in the layout and processing of meat products. In the future, it is expected to gradually focus on large-scale agricultural enterprises.

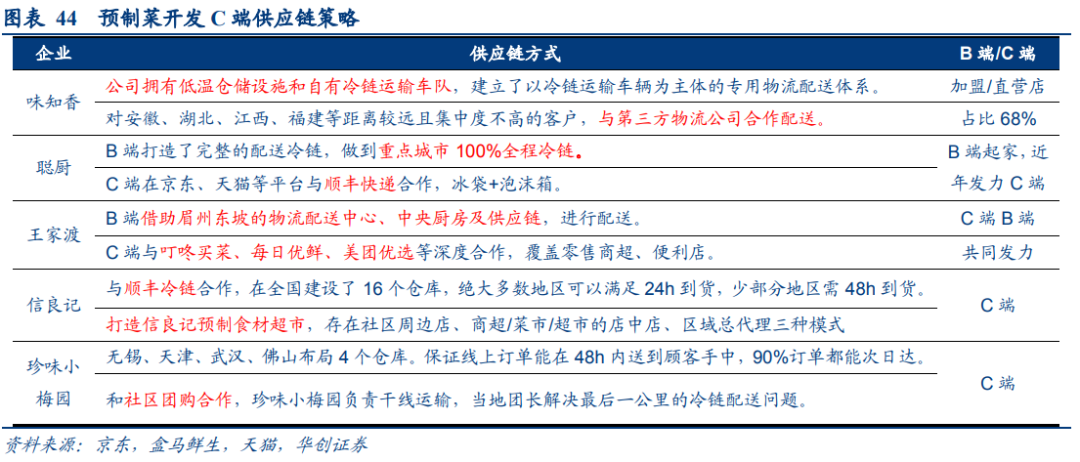

4. C-end: Demand still needs to be cultivated, and competition is relatively scattered

The C-terminal needs to bear the cost of consumer education, making it more difficult to operate, and early entrants often fail.

The C-end consumers are poorly educated, the demand side is changing rapidly, and they are facing supply chain challenges (scattered demand points, high transportation costs, vulnerability, etc.), making it difficult to increase their overall sales volume. At the same time, early entrants mostly entered in the form of heavy assets. A batch of semi-finished food companies such as Youth Cuijun and Our Kitchen, which emerged in the 13th and 14th years, are extremely vulnerable to the risk of capital breakage under uncertain demand conditions.

Most new entrants choose to focus on the lower threshold C-end. Due to the diversification of C-end marketing and the blurring of channels, enterprises mostly focus on Internet marketing, focusing on product innovation, iteration speed, and dissemination attributes. In terms of research and development, choose to restore online red dishes, local specialties, or store hot items; Marketing focuses on community marketing and scene marketing, such as live streaming, online red grass planting, etc.

The farmers' market has a fixed consumer base, strong purchasing purpose, and high conversion rate. It achieves the collection of C-end volumes, improves supply chain efficiency, and relies on offline centralized exposure to facilitate face-to-face consumer education and training for prefabricated dishes. It is currently a relatively mature business model. Other modes of supply chain are still being explored, and third-party platforms are often selected for cooperation, but the actual effect remains to be observed.

.END.

.END.